A TIIN is supposed to answer seven questions. (They are here in the TIIN instructions – the TIIN instructions still aren’t published by HMRC – and why not??? – but let’s assume the basic principle is still the same as “in my day”.)

The questions are:

What are you doing?

Why are you doing it?

Why are you doing it this way?

What will it cost/raise?

What will it cost the customer?

What will it cost the department?

Are there any other impacts?

“Why are you doing it” is a powerful question in the “better regulation” mindset, which basically reflects a worldview in which regulation is a Bad Thing in and of itself. The idea is that regulation is nothing more than Red Tape, which would be Strangling Business unless it was itself regulated. “Why are you doing it (at all)” is really the question, if you think that having no regulation at all is the ideal.

So why is the government doing MOSS at all? Well let’s see. The policy objective field of the TIIN (still on page A111) is where the answer ought to be, and it says:

Policy objective The measure will make business to consumer (B2C) supplies of BTE services taxable where they are consumed, thereby removing an incentive for businesses to locate offshore. This will level the playing field for UK BTE suppliers and is consistent with the Government’s aim of fairness in the tax system. The MOSS business simplification scheme is intended to reduce the administrative burdens and costs associated with this rule change and multiple VAT registrations for BTE suppliers, particularly for small and medium enterprises (SMEs).

Translated into English, I think this means there are two objectives:

- The main objective is to stop big companies from gaming the system by setting up shop somewhere with a low VAT rate. Instead of VAT being charged where the supplier is located, from January 2015 it is charged (for electronic services like e-books) where the customer is located. So small companies should have a more “level… playing field… consistent with the Government’s aim of fairness…”

- Because this change comes with associated costs for small companies, there will also be the “mini one stop shop”, the MOSS, which stops you having to register for VAT separately in each member state and instead handles it all in once place, the place the seller is located.

Now, I think the objectives are good ones in themselves. Let’s make it easier for authors to sell their own works, for craftswomen to sell their own knitting patterns, for musicians to sell their own tunes, directly to the customer without having to lose a slice of their profits to a multinational selling for them. And, yes, let’s keep the administration as simple as possible.

So what went wrong?

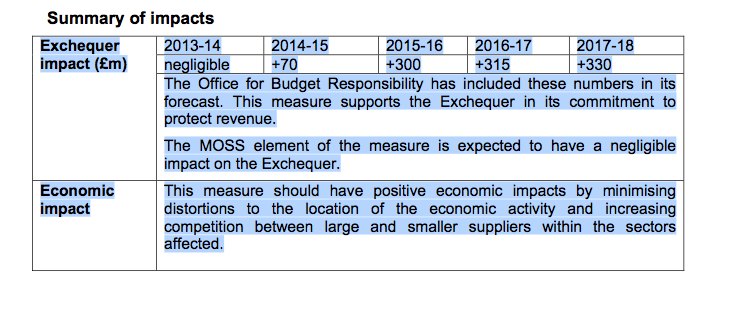

Let’s go back to the TIIN, to the summary of impacts that starts at the bottom of page A112.

The first line shows you how much money the government expects to get as a result of this change. The numbers are in millions of pounds, and the plus sign means the government expects to get this much tax in from the change.

The first few months of 2015 are still in the 2014-15 tax year (the tax year runs from 6th April one year to 5th April the next year). So between January 1st and April 5th 2015 the UK government estimates it will make £70 million in VAT from the changes. In a full year, it thinks it will make an extra £300 million plus, with the numbers rising over time.

I think we can all agree three hundred million is a sum worth having. For the government, it’s the cost of, say, the entire NHS radiotherapy service (table 9 page 28, 2011-12 figures). But look at this: “The MOSS element of the measure is expected to have a negligible impact on the Exchequer.”

Now, I understand “negligible” in an impact assessment to mean “less than £100,000 across the entire affected population”, which is what it used to mean in 2012 when I was last working for the government. But have a think about that. The entire farrago of MOSS is expected to bring in less than a hundred grand? Seriously?

Because one of the seven questions written into the tax original impact assessment proposals, and which was still there when I obtained the TIIN instructions and published them on my blog, is

why are you doing it this way???

Why the hell are you imposing this business-busting system on people from whom you expect to raise peanuts, when you’re still going to get the moolah you want from the big businesses it’s really aimed at? Is this really the only way?

Option appraisal is one of the key elements of impact assessment methodology: generating and assessing all the possible ways of solving a possible policy issue and then choosing the best one, even if it’s the option to “do nothing” – that’s how governments tell themselves they solve problems.

So where is the options appraisal in this TIIN?

Don’t bother to look. It isn’t there.

Look instead at the assessment of the economic impact.

This measure should have positive economic impacts by minimising distortions to the location of the economic activity and increasing competition between large and smaller suppliers within the sectors affected.

Well perhaps it “should”. In an ideal world it would. But in this imperfect world, HMRC completely overlooked the one-woman kitchen-table microbusiness and introduced a system which, far from “minimising distortions” and “increasing competition” will in fact wipe out the micro businesses or else drive them into the arms of the very businesses whose behaviour caused the policy problem in the first place.

A proper options appraisal might have included:

- excluding micro businesses from the regulation altogether

- allowing a longer lead in time before the regulation affected small and micro businesses

- unilaterally setting a threshold below which the regulations do not apply

- making payment processors legally responsible for operating the regulation

- devising a MOSS which itself operated as a payment processor for micro businesses (instead of a paypal or worldpay etc button you could have a MOSS button – your money would come to you VIA the government, but come to you guaranteed VAT-compliant)

There might have been good reasons for and against any or all of these. But if you don’t ask the right questions of the right people, well, you’ll never know, will you?